Debt Literacy Month: Nearly Half of Canadians Express Regret Over Debt as Financial Blind Spots Endure

As economic pressures continue to mount across the nation, comprehensive five-year tracking data compiled by Ipsos on behalf of MNP LTD reveals a troubling financial landscape for Canadians. The findings, released during Debt Literacy Month, indicate that debt concern remains persistently elevated, financial preparedness has noticeably declined, and significant gaps in debt literacy continue to leave many households vulnerable to common financial shocks and the long-term consequences of borrowing costs.

Persistent Debt Anxiety Across Generations

The national survey data demonstrates that more than two in five Canadians (44%, representing a 2 percentage point increase from 2020) express concern about their current level of debt. Perhaps more strikingly, nearly half of all Canadians (47%, also up 2 percentage points from 2020) report regretting the amount of debt they have accumulated over their lifetime. This sentiment of financial remorse has become increasingly prevalent as economic conditions have evolved.

Confidence in long-term financial stability remains fragile across the population, with only half of Canadians (51%, down 2 percentage points from 2020) expressing belief that they will achieve debt-free status by retirement. This uncertainty about future financial security highlights the profound impact that current debt burdens are having on Canadians' long-term planning and peace of mind.

Generational Divide in Debt Concerns

The data reveals particularly pronounced debt anxiety among younger generations, who face unique economic challenges. Concern about current debt levels is highest among Generation Z respondents (55%, representing a substantial 13 percentage point increase from 2020) and Millennials (55%, unchanged from 2020). This heightened concern reflects the particular financial pressures facing younger Canadians as they navigate housing costs, education expenses, and career establishment in a challenging economic environment.

Perhaps most telling is that three in five Millennials (59%, up 2 percentage points from 2020) report regretting the amount of debt they have taken on throughout their lives, representing the highest level of debt regret among any age demographic. This generational pattern suggests that younger Canadians are experiencing particularly acute financial stress and reconsideration of their borrowing decisions.

The Persistent Debt Literacy Gap

Despite increased borrowing becoming more commonplace amid sustained cost-of-living pressures, many Canadians continue to demonstrate limited understanding of fundamental financial concepts. The survey reveals that one in five Canadians (20%, though this represents a 5 percentage point improvement from 2020) still lack a solid understanding of how interest rate increases impact their personal financial situation. While this indicates modest progress in financial education over the five-year tracking period, it simultaneously highlights that significant knowledge gaps persist across the population.

"The data underscores the critical need for stronger debt literacy initiatives across the country," emphasizes Grant Bazian, president of MNP LTD, Canada's largest insolvency firm. "Simple awareness of outstanding balances is insufficient in today's complex financial environment. A practical, working understanding of compounding interest mechanisms, rate sensitivity implications, and contingency planning strategies has become increasingly essential for financial resilience."

The Compounding Consequences of Financial Illiteracy

Bazian further explains the long-term implications of debt literacy gaps: "The compounding effect of interest can carry significant consequences that accumulate quietly over time. Throughout a five-year period, for instance, debt can function like financial quicksand—borrowing costs compound gradually, and even seemingly modest rate increases can substantially deepen the overall burden as time progresses. What begins as manageable debt can gradually extend repayment timelines and dramatically inflate the total interest paid over the life of the obligation."

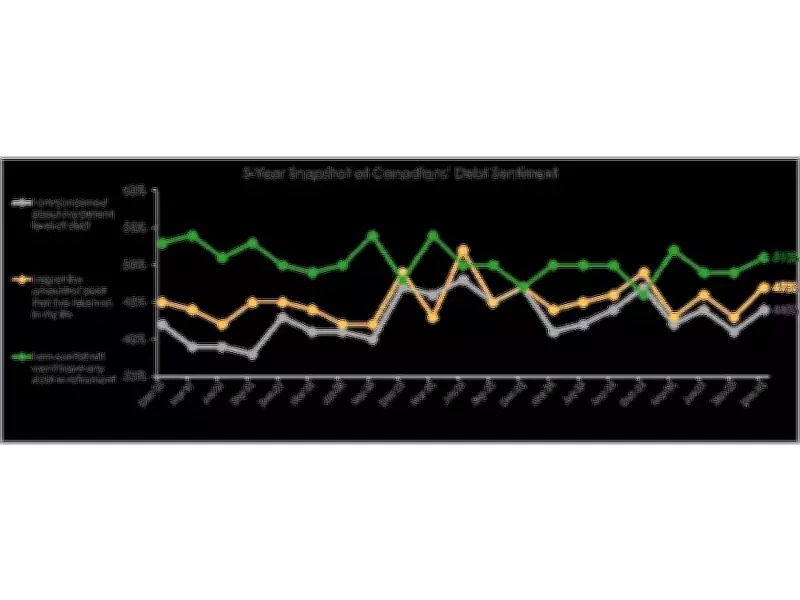

Evolving Financial Sentiment Patterns

The longitudinal data reveals interesting patterns in Canadian financial sentiment over time. Beginning in 2022, measures of debt concern, debt regret, and confidence in achieving debt-free retirement have shown greater quarter-to-quarter variation, consistent with a period of broader economic adjustment and uncertainty. However, in the 2024-2025 period, these three key indicators have moved within a narrower range than in previous years, suggesting less separation between Canadians' perspectives on their past borrowing decisions, present financial situations, and future debt expectations.

This convergence of financial sentiment indicators may reflect a normalization of debt as an ongoing feature of Canadian household finances, even as regret and concern remain elevated. The findings collectively paint a picture of a population grappling with the practical realities of debt management while simultaneously lacking the comprehensive financial literacy needed to navigate these challenges effectively.

The persistent debt literacy gaps identified in the research leave many Canadians financially vulnerable to unexpected economic shocks and the long-term implications of borrowing decisions. As economic conditions continue to evolve, the need for practical financial education that addresses real-world debt management challenges becomes increasingly urgent for households across the country.